Home / Fixed Deposit

Designing the premier low-risk investment product on the market

Product Design, Service Design, Financial

Product

Guaranteed Investment

Certificates

Client

Scotiabank Colombia

Date

2018

Guaranteed Investment Certificates (GICs) are a financial product that allow customers to invest their funds for a fixed term at a variable interest rate. Funds invested in a GIC cannot be withdrawn prior to the maturity date, at which point the initial investment is returned along with the accrued interest earned during the term. GICs may also be referred to as Certificados de Depósito a Término (CDTs) in Spanish.

The challenge

In 2018, Scotiabank in Colombia did not have a digital process for opening GICs. This required customers to visit a physical branch and spend an average of two hours to complete the process.

The goal

As part of the bank's digital transformation efforts, my team was tasked with creating an online version that would allow new and existing customers to open term deposits from any location at any time.

My role

As the Senior User Experience Designer, it was my responsibility to design an end-to-end experience that balanced the needs of the users and the business goals.

User Research

To gain a deeper understanding of the problems and needs of our target audience, I worked with the bank's research team to develop hypotheses and conduct user research. This included benchmarking against other financial institutions, interviews with current and potential customers, and a card sorting exercise to understand mental models for the product. I also had access to data from the existing product and the market. For instance, one of my initial assumptions was that the better the interest rate, the more likely we would sell the product (wrong!).

During the research process, it was discovered that most customers did not choose the bank with the highest interest rates for GICs. Instead, other factors motivated their decisions (as detailed in the Takeaways and Findings section).

Research Activities

To gain a comprehensive understanding of the financial sector, both domestic and international benchmarks were conducted. This included analyzing the offerings of 15 financial institutions in Colombia and 15 institutions globally. This competitor analysis informed the design of the first draft of the Information Architecture.

Interviews were then scheduled with current customers who had the product, as well as potential customers who had not yet acquired it. These interviews concluded with the creation of empathy maps, which captured the needs, motivations, fears, and expectations of each user. User personas were then developed based on the qualitative data obtained through these interviews.

In addition, a card sorting exercise was conducted to understand the mental models that people had for the product.

The analysis of this data provided valuable insights and contributed to the early findings.

The example above was taken from the card sorting activity

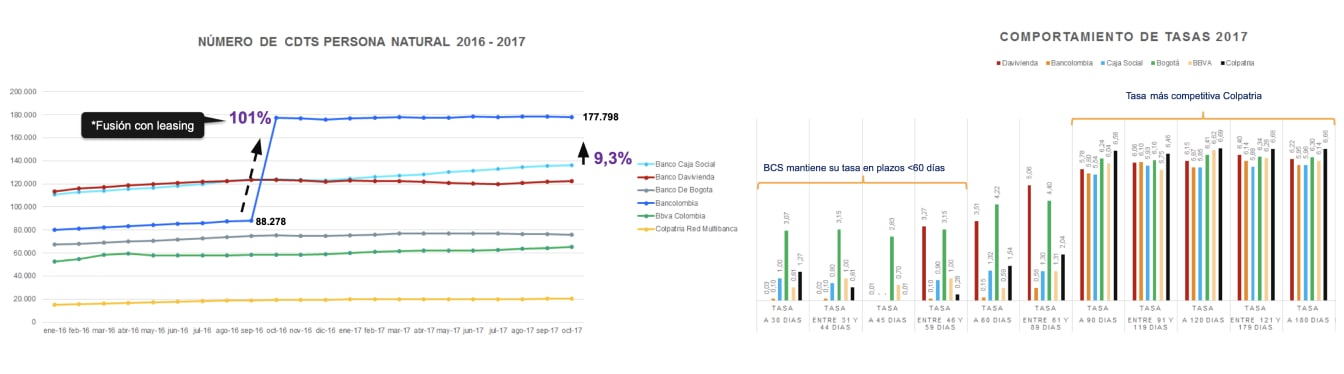

Finally, it was fortunate to have a full-time data scientist on the team, providing access to data on the current offline product and the market.

Source: Superfinanciera de Colombia

Pain Points

In the early phase of the project, an understanding of the pain points experienced by customers was gained through empathy and analysis. The top three identified pain points were:

Time-consuming process

The lengthy time required to open

a Fixed Deposit at a branch was identified as a major barrier for customers.

Withheld funds:

Customers were unable to access

their funds before the maturity date, which was a source of frustration.

Extensive paperwork

The complexity of the required

paperwork was a common complaint among customers, making the product seem unnecessarily

complicated.

User Persona #1

Manuel

Age 46

Occupation Sales Manager

Salary $3.000 USD / month

Financial Products Credit Cards, Chequing Account, Mortgage, Fixed Deposit

When evaluating GICs, the best interest rates are the primary factor I consider

Goals

This individual's primary goal is maximizing profitability. They constantly search for the highest interest rates at various banks.

Frustrations

The absence of simulators and comparison tools for all banks, as well as the lack of personalized service and custom alerts for their investments, are sources of frustration for this individual.

Journey / Satisfaction Map

User Persona #2

Gloria

Age 57

Occupation Accountant

Salary $1.500 USD / month

Financial Products Credit Cards, Chequing Account, Savings Account

As I am saving for my son's college education and do not have a strong savings habit, I must discipline myself to avoid accessing my savings

Goals

This individual desires to regularly save money and keep it separate from their regular expenses.

Frustrations

Debt presents significant challenges for this person in terms of saving or investing.

Journey / Satisfaction Map

User Persona #3

Lorena

Age 29

Occupation Psychologist

Salary $1.600 USD / month

Financial Products Credit Cards, Chequing Account, Savings Account

Saving has always been a priority for me, as it was instilled in me by my parents. It is always important to ensure that savings are secure in a bank.

Goals

This individual's goals include growing their savings and automating their saving process.

Frustrations

This person finds it frustrating to spend time on tasks that should be easily completed online in a short period of time.

Journey / Satisfaction Map

The Design

To create the first wireframes, a comprehensive list of features and content gathered during the Understanding and Specify phase was compiled.

It was necessary to refine this list through extensive discussions with the Product Owner (PO), stakeholders, and team members. The regulatory requirements of the MVP presented some challenges in these negotiations. The PO was instrumental in addressing complex compliance questions and advocating for the needs of the users. For example, we eliminated the need for an in-person signature and a printed certificate of ownership. Other requests and items, such as product offerings based on a yearly schedule, were also removed.

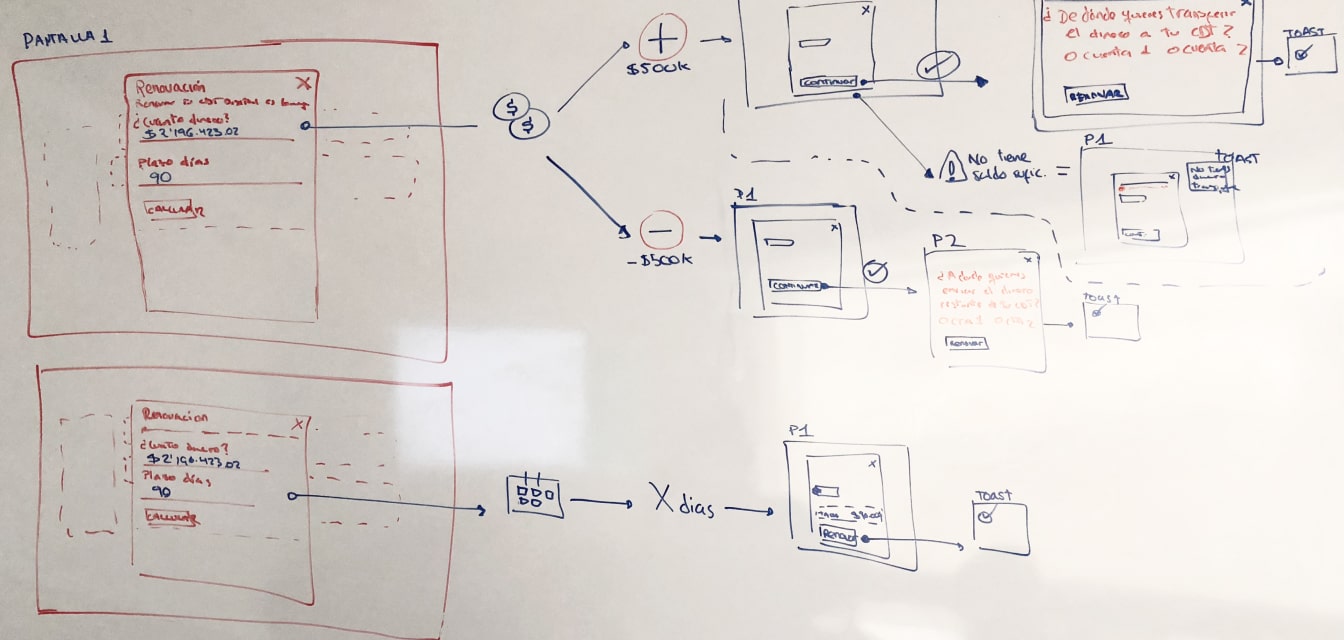

First prototype

Since it was assumed that the majority of user personas would access the GIC via smartphone, the first prototype focused on the mobile version.

Usability testing was divided into three chapters, representing the lifetime of the product: opening, product information, and renewal/termination. For each chapter, the researcher provided context (a scenario) to the participant before assigning tasks.

Takeaways and Findings

Here are some key takeaways from this project:

Interest rates are not always the primary

consideration

Some users preferred to receive

an immediate benefit, such as a gift, when opening a Fixed Deposit. Others simply wanted to secure

their money with a trusted institution for a specific period in order to achieve a specific

goal

Simulators are crucial

Users desire the ability to

determine the interest rate and profitability before making a purchase.

Low investment amounts are attractive to

customers

Many customers emphasized the

importance of being able to invest small amounts, even if it is less profitable. This insight

presented a valuable marketing opportunity.

The MVP launch resulted in exceeding the customer acquisition goal by 32.5% in the first month. The focus on the user experience from the outset contributed significantly to this positive outcome.

In addition to traditional advertising and promotion techniques, innovative methods were utilized to attract new clients. For example, food vouchers were offered to the first 150 customers who signed up for a term deposit, which proved to be a successful strategy.

Finally, it is essential to continuously optimize the user journey and make it more efficient, allowing the user to complete tasks in fewer steps. The team's efforts in this regard have contributed to the ongoing success of the product and the satisfaction of customers.